What if your strong personal credit score could help you access large amounts of business funding without paying interest or risking your personal assets every time?

For entrepreneurs with a 725+ score, the door to 0% APR business credit cards is wide open, offering a way to fund growth using your Employer Identification Number (EIN). In this guide, you will learn how to leverage your creditworthiness to access high-limit, interest-free funding.

By focusing on 0% APR business credit cards, you can bridge cash flow gaps and scale your operations without the burden of immediate interest.

How a 725+ Score Opens Access to 0% APR Business Credit Cards

While many business owners dream of an EIN-only business credit card, the reality is that the most lucrative interest-free offers usually require a “Personal Guarantee” (PG) initially. However, there is a massive silver lining: when you have a score above 725, banks view you as a low-risk partner.

This allows you to secure 0% APR business credit cards that often do not report to your personal credit bureau, keeping your personal debt-to-income ratio pristine while you build your business empire.

A high score doesn’t just get you an approval; it gets you the highest possible limits. When applying for 0% APR business credit cards, a 725+ score can be the difference between a $5,000 limit and a $50,000 limit. This capital is essentially a “free loan” from the bank for 12 to 18 months, depending on the intro APR terms provided by the issuer.

If you want to understand EIN-only business credit in detail and learn how approval works, this guide breaks it down step by step.

What We Commonly See Business Owners Get Wrong

One of the biggest misconceptions about 0% APR business credit cards is that the introductory offer is the most important factor.

In practice, we often see business owners focus on the promotional rate while overlooking repayment strategy, cash flow management, and long-term financing goals.

Some of the most common mistakes include:

- Applying before the business is financing-ready

- Carrying balances beyond the promotional period

- Using credit cards to solve recurring cash-flow problems

- Focusing on credit limits instead of repayment capacity

- Ignoring business credit development while relying solely on personal credit

A promotional financing offer can be valuable, but it works best when it is part of a larger financial strategy.

Understanding EIN-Only vs. Personal Guarantee Options

If you are specifically looking for a no personal guarantee business card, you are likely looking at the world of corporate cards. These cards function differently than traditional revolving credit.

Corporate Cards EIN Path

For established businesses with significant revenue, corporate cards EIN applications are the standard. These cards, such as those from Brex or Ramp, do not require a personal credit check or a personal guarantee. Instead, they look at your business’s cash balance and monthly revenue.

The Hybrid Strategy

For most small to mid-sized business owners, the “Hybrid Strategy” is more effective. You use your 725+ personal score to qualify for 0% APR business credit cards from major lenders like Chase, American Express, or Bank of America.

Even though you provide a personal guarantee, these cards report only to the business credit bureaus (like Dun & Bradstreet or Experian Business). This allows you to use the credit for your EIN while protecting your personal score from high utilization.

What We Look For Before Recommending a Business Credit Card in 2025 and 2026

Credit card offers change constantly.

Instead of focusing on specific products, we typically evaluate:

- Introductory APR duration

- Annual fees

- Reporting behavior

- Credit limit potential

- Business credit reporting

- Underwriting requirements

- Cash-flow needs

- Long-term financing goals

The right card depends on the business, not the advertisement.

Top Interest-Free Business Cards Comparison

| Card Name | Intro APR Duration | Annual Fee | Best For |

| Amex Blue Business Plus | 12 Months | $0 | General spending & Rewards |

| Chase Ink Business Unlimited | 12 Months | $0 | Flat-rate cash back |

| U.S. Bank Business Platinum | 18 Months | $0 | Longest interest-free period |

| PNC Visa Business | 13 Months | $0 | Consistent cash flow management |

The Amex Blue Business Plus remains a fan favorite because it offers 2x points on the first $50,000 spent annually, combined with a solid interest-free period. When you use 0% APR business credit cards like these, you can buy inventory, pay for advertising, or cover equipment costs today and pay them back over the next year without a penny in interest.

Business Credit Card Requirements for High-Limit Approvals

Getting approved with your EIN isn’t just about your score. You must meet specific business credit card requirements to ensure the bank sees your company as a legitimate entity.

- Legal Formation: You should have an LLC, S-Corp, or C-Corp. While sole proprietors can get these cards, having a formal structure makes you look more professional to underwriters.

- Business Bank Account: Lenders want to see that you are not co-mingling funds. A dedicated business checking account is a must.

- Professional Presence: A business phone number, a professional email (not @gmail.com), and a basic website can significantly increase your approval odds.

- Clean Personal Credit: Ensure your 725+ score doesn’t have recent late payments or high personal utilization (under 30% is ideal).

By meeting these business credit card requirements, you position yourself to receive the most competitive 0% APR business credit cards on the market.

Strategic Use of Intro APR Terms

One of the most important aspects of managing your business finances is understanding the intro APR terms. A 0% offer is a powerful tool, but it is not a “set it and forget it” solution.

- The Expiration Date: Always mark the month the 0% period ends. If you carry a balance past this date, the interest rate can jump to 16%–28% instantly.

- Minimum Payments: You must still make the minimum monthly payment. Failing to do so can void your 0% offer and damage your credit score.

- The “Debt Shuffle”: Many savvy entrepreneurs use 0% APR business credit cards to pay off high-interest debt or to fund a project that will generate ROI before the intro period expires.

Pro Tip: If you have a massive project that will take 18 months to pay off, prioritize cards like the U.S. Bank Business Platinum, which often features the longest durations in the industry.

A Real-World Observation

One contractor we reviewed needed equipment for a busy season but wanted to avoid high-interest financing.

Rather than pursuing a short-term loan, the owner used a promotional business credit card to cover the purchase and structured repayments around incoming contract revenue.

Because the balance was repaid before the introductory period expired, the company was able to improve cash flow without incurring interest charges.

The strategy worked because repayment planning occurred before the purchase—not after.

(Certain details have been modified to protect client privacy.)

What We Review Before Recommending a Business Credit Card Strategy

Before recommending a financing approach, we typically review:

- Personal credit profile

- Business revenue

- Banking activity

- Existing debt obligations

- Credit utilization

- Time in business

- Industry risk

- Financing goals

A strong credit score is helpful, but lenders often evaluate a much broader financial picture.

Why Lenders Look Beyond Credit Scores

A strong score does not automatically create the strongest financing profile.

For example:

| Metric | Business A | Business B |

|---|---|---|

| Personal Credit Score | 760 | 730 |

| Monthly Revenue | $8,000 | $35,000 |

| DSCR | 0.90 | 2.10 |

| Banking Activity | Average | Strong |

| Existing Debt | High | Moderate |

Although Business A has the higher score, many lenders may prefer Business B because stronger cash flow often represents lower overall lending risk.

Credit scores matter.

Cash flow often matters just as much.

Building an EIN-Only Profile with No Personal Guarantee

If your goal is to eventually move away from personal guarantees entirely, you must use these cards to build your business credit profile. While you enjoy the benefits of 0% APR business credit cards, your on-time payments are being reported to business credit bureaus.

Once your business has a strong “Paydex” score (Dun & Bradstreet) or a high Experian Business score, you can apply for a no personal guarantee business card with much higher success. Companies like Divvy (now BILL) and Ramp provide excellent platforms for managing spending once your business has established its own credit identity.

These corporate cards EIN options are the “end game” for many founders who want to completely decouple their personal finances from their business risks.

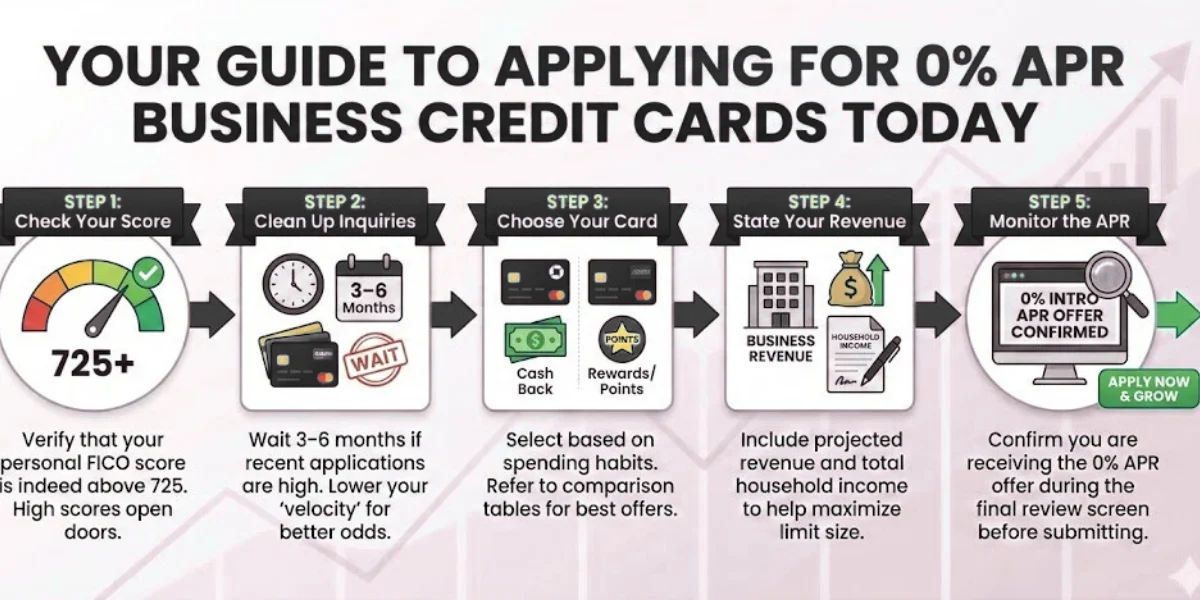

How to Apply for 0% APR Business Credit Cards Today

Ready to take action? Follow these steps to maximize your chances:

- Check Your Score: Verify that your personal FICO score is indeed above 725.

- Clean Up Inquiries: If you have applied for many cards recently, wait 3–6 months to ensure your “velocity” isn’t too high.

- Choose Your Card: Based on the table above, select the card that fits your spending habits (e.g., Chase for cash back, Amex for points).

- State Your Revenue: Don’t be afraid to include projected revenue or your total household income if the application allows it. This helps with limit size.

- Monitor the APR: Confirm you are receiving the 0% APR business credit cards offer during the final review screen of the application.

Conclusion

Lessons Learned

After reviewing financing profiles across multiple industries, several patterns appear consistently:

A High Credit Score Creates Opportunities

Strong personal credit may improve access to financing options, but it is rarely the only factor lenders evaluate.

Promotional Financing Requires a Plan

Businesses that create repayment strategies before borrowing often experience better outcomes than those focused solely on approval.

Cash Flow Remains Critical

Even with a 0% APR offer, repayment capacity remains one of the most important factors in long-term financial success.

Financing Readiness Extends Beyond Credit

Business banking activity, revenue consistency, vendor relationships, and financial management all contribute to future financing opportunities.